Article

The United States (US) is forming resource partnerships in Southeast Asia, through bilateral critical minerals agreements, such as memoranda of understanding (MOUs) and agreements on reciprocal trade (ART), as well as through the Forum on Resource Geostrategic Engagement (FORGE), a US-led multilateral framework that is reshaping the value capture, control, and risk associated with the regional supply chains.

While these arrangements are presented as mutually beneficial, they have thus far indicated stronger gains for the US' strategic and supply security objectives than for industrial benefits for producing countries. Without stronger commitments on investment, processing capacity and governance, benefits are likely to remain unevenly distributed.

Click to download the explainer and infographics.

Key points

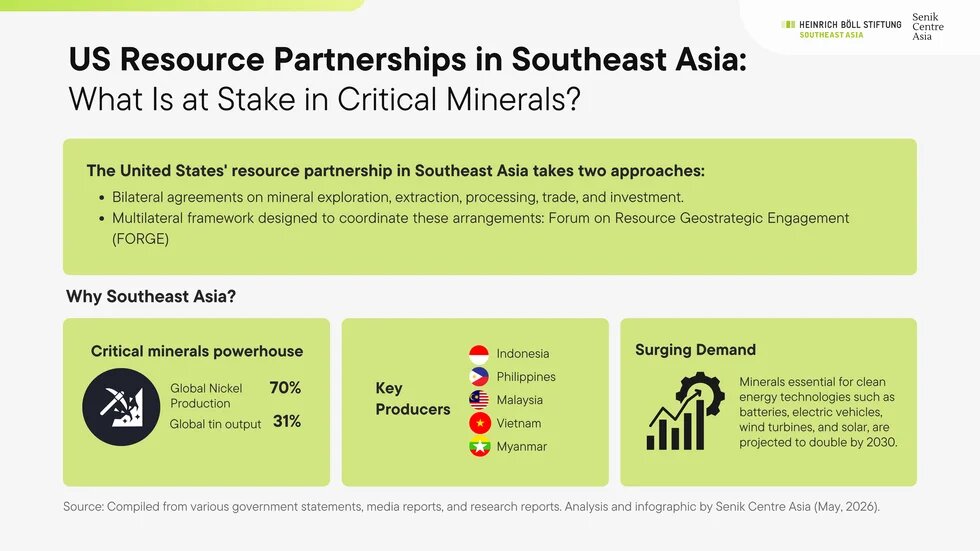

- The United States' resource partnerships in Southeast Asia take two approaches: bilateral critical minerals agreements with Southeast Asian governments, and the Forum on Resource Geostrategic Engagement (FORGE), a separate multilateral framework designed to coordinate these arrangements.

- Since late 2025, the US has reached several bilateral critical minerals agreements with countries in Southeast Asia. Most of these are non-binding government-to-government MOUs that signal intent but do not legally obligate either party to provide financing, technology transfer, or changes in processing ownership.

- China still anchors much of Southeast Asia’s critical mineral-related facilities through investment, technology, and market share. Without stronger provisions regarding local value addition and non-Chinese ownership as well as operation, it is unlikely that the new US arrangements will shift control over key processing facilities in the near term.

- FORGE (Forum on Resource Geostrategic Engagement) aims to coordinate pricing and trade rules, including reference prices and price support mechanisms, to ensure the commercial viability of mineral projects aligned with the US. Its design relies on tariff authorities and price floor mechanisms, which are still legally and politically uncertain.

- Agreements are being made at a faster pace than the governance needed to manage extraction and refining risks. Safeguards relating to social-environmental, community protections, and transparency and accountability remain limited.

- Without binding commitments on processing, investment, and ownership, producing countries are likely to remain as commodity suppliers. Meanwhile, the US and other advanced industrial economies will primarily benefit from increased industrial value added and supply-chain security.

What are US bilateral resource partnerships, and why Southeast Asia?

US bilateral resource partnerships are government-to-government agreements on mineral exploration, extraction, processing, trade, and investment that are largely meant to secure critical mineral supply chains for national security and competitiveness. These range from non-binding memoranda of understanding (MOUs) that do not create legally enforceable commitments for the US or partner governments to enforceable trade agreements including tariff schedules and investment rights.

Southeast Asia has key mineral resources that are critical to a diversified supply chain strategy. Indonesia produces more than half of the global nickel supply. The Philippines is the world’s second-largest nickel producer. Malaysia hosts the only commercial-scale heavy rare earth separation facility outside China. Vietnam holds the sixth-largest rare earth reserves globally, at 3.5 million tonnes, while Myanmar is the world’s third-largest producer of rare earth elements. ASEAN accounts for around 70% of global nickel production and around 31% of the tin supply, making the region an important node in the global mineral[1] supply chain.

International Energy Agency (IEA) Global Critical Minerals Outlook 2024 estimates that under a Stated Policies Scenario[2] demand for minerals used in clean energy technologies could double by 2030 and nearly quadruple by 2040 on a net-zero pathway[3]. Demand for critical minerals such as nickel and rare earths is projected to increase significantly, driven mainly by the rapid uptake of electric vehicles and clean energy deployment.

Why is Southeast Asia so contested amid China’s dominance?

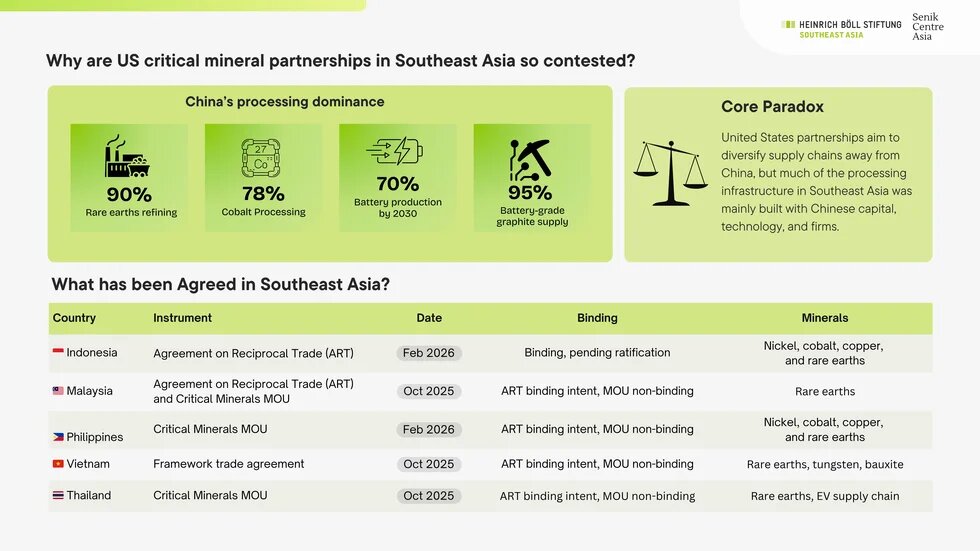

China is the dominant player across the global critical mineral supply chain. China controls around 70% of the global rare-earth mining and approximately 90% of the refining capacity, which gives it significant leverage over critical mineral supply chains. China is the world’s leading cobalt refiner and processes around 78% of global supply, despite the Democratic Republic of the Congo (DRC) holding the largest reserves.

By 2030, China is expected to remain as the dominant hub of the EV battery supply chain, with around 70% of announced battery production capacity located in the country. Battery-grade graphite supply is even more concentrated, with China will be meeting around 95% the incremental demand growth.

China has utilised its dominance related to critical minerals and clean energy supply chain to gain strategic leverage. In April 2025, China introduced export restrictions on seven rare-earth elements following a new round of US tariffs. By October 2025, the restrictions were expanded to include foreign firms exporting products containing more than 0.1%. Although some controls were temporarily eased in November for one year, the direction of policy still indicates a tendency to use supply chain as a strategic lever.

This pattern of influence extends also to Southeast Asia, where Chinese investment has created deep structural dependencies. For example, Myanmar, the world’s fourth-largest rare earth producer, supplies much of its output to China’s processing base. Meanwhile, over 65 billion US dollars investments have flowed into Indonesia’s nickel sector. China’s firms also control approximately 75% of refining capacity while Indonesian-owned enterprises hold only 13% of nickel refining capacity. Analysts estimate that roughly 10% of nickel profits ultimately accrue to Indonesian companies. China’ role goes even deeper with more than 70% of the heavy machinery used for minerals ore and almost 90% refining machinery for Indonesia’s nickel sector comes from Chinese suppliers.

This concentration of ownership and value capture creates a core constraint and paradox for the current US bilateral strategy. The regional agreements aim to diversify supply chains away from China, but the processing infrastructure they depend on remains predominantly Chinese-built and operated. In practice, the absence of binding investment and ownership in these agreements constrains their ability to build greater influence and shift control over processing and supply chains in the near term.

How the Hormuz shock shifts the frame |

|

Amid the escalating Middle East crisis, the effective closure of the Strait of Hormuz in March 2026, has forced a global rethink of what energy security and the clean energy transition mean, with oil prices rising above 120 US dollars per barrel and global fuel markets tightening. This will shape how governments define energy security, especially given the current global fiscal stress, taking it beyond a fossil-fuel lens. The crisis has highlighted the importance of clean energy transitions as key aspects of resilience. In turn this has made secure access to critical minerals and processing capacity a central part of the energy security discussion, rather than just a climate concern. |

What has been agreed across US bilateral critical minerals partnerships in Southeast Asia?

The US established five bilateral agreements in Southeast Asia between October 2025 and February 2026. Each agreement differs in terms of legal form, mineral focus, and implications for domestic processing and value capture. Overall, the arrangements remain fragmented, with varying commitments on investment, processing and ownership across both binding and non-binding agreements.

Table 1: US Bilateral Critical Minerals Arrangements in Southeast Asia (2025–2026)

| Country | Instrument | Date | Status | Key minerals | Processing stance |

| Indonesia | Agreement on Reciprocal Trade (ART) | Feb 2026 | Binding, pending ratification. | Nickel, cobalt, copper, and rare earths | Downstreaming is preserved in principle; contested |

| Malaysia | Agreement on Reciprocal Trade (ART) and critical minerals MOU | Oct 2025 | ART binding intent, MOU non-binding | Rare Earths | Raw rare earth export curbs maintained |

| Philippines | Critical minerals MOU | Feb 2026 | ART binding intent, MOU non-binding | Nickel, cobalt, copper, rare earths | Local processing is explicitly targeted |

| Vietnam | Framework trade agreement | Oct 2025 | ART binding intent, MOU non-binding | Rare earths, tungsten, bauxite | Raw rare earth exports banned from Jan 2026 to push processing |

| Thailand | Critical minerals MOU | Oct 2025 | MOU non-binding | Rare earths, EV supply chain | Downstream processing and EV assembly focus |

Source: Compiled from government statements, treaty texts, media reports, and research analysis, including White House, USTR, Philippine Embassy, Washington, US Mission to ASEAN, Bloomberg coverage of Vietnam’s rare earth export ban, and analysis by Senik Centre Asia.

Indonesia: binding deal and asymmetrical obligations

The Agreement on Reciprocal Trade (ART), signed on 19 February 2026, imposes a 19% tariff on Indonesian goods whilst Indonesia eliminates tariffs on over 99% of US products. As part of the negotiations, Indonesia has committed to remove restrictions on the export of processed critical minerals to the US market. This will enable a package of commercial arrangements valued at about $33 billion. This includes a $20 billion Freeport-McMoRan Grasberg mining license extension to the year of 2061.

The government has further argued that the ART preserves its national strategic project to develop the natural resources downstreaming, claiming that the clause on export restrictions clause applies only to minerals that have already undergone secondary processing. However, Indonesian civil society groups view the agreement differently. The civil society coalition has since lodged a lawsuit at the Jakarta Administrative Court. The formal objection mainly argues that the agreement places a disproportionate share of binding obligations on Indonesia relative to the US[4] and seeks suspension of ratification as the agreement could weaken Indonesia’s bargaining power over its resources.

Philippines: processing ambitions and governance gaps

The Philippines–US MOU, signed on 4 February 2026 by the Secretary of the Department of Environment and Natural Resources (DENR) and US Undersecretary, explicitly prioritise domestic processing over the raw ore exports. The Philippines has an estimated 1 trillion US dollars’ untapped mineral and world’s second-largest nickel producer. Over 87% of Philippine nickel ore is exported to China and the country’s only operates two HPAL plants, both of which are Japanese-owned.

Through the partnership, the Philippine government seeks to increase domestic processing and shift value capture onshore. However, the MOU is non-binding, and contains no firm investment commitments. It also lacks a formal Critical Minerals Agreement designation, meaning Philippine minerals are not automatically treated as “trusted” under US law. This makes it harder to build downstream processing at scale.

There are also concerns about weak oversight of the sector, with the DENR failing to adequately regulate mining. As seen in communities such as Caraga, where protections remain insufficient despite the operation of 23 nickel mines.

Malaysia: contested heavy rare earth refining role

Malaysia plays a key role in the global rare earth supply chains, primarily through the Lynas Advanced Materials Plant (LAMP) in Pahang. LAMP is the only commercial facility in the world outside China that processes heavy rare earth elements (including dysprosium and terbium). Lynas has also finalised a four-year, $96 million US Department of Defence supply contract, which further embeds the plant in non-Chinese rare-earth supply chains.

At the October 2025 ASEAN Summit, Malaysia signed both an ART and a critical minerals MOU with the US, whilst maintaining its ban on raw rare earth exports. China has also engaged with Malaysia through parallel arrangements, positioning Malaysia as a contested node in competing supply chain strategies rather than as a straightforward US partner.

Vietnam: export controls and leverage

Vietnam has the world’s sixth-largest rare earths reserve and is also a major producer of tungsten. Despite its strategic position in critical mineral supply chains, Vietnam has not established a specific critical minerals agreement with the US, instead focusing on broader economic and strategic cooperation frameworks.

In December 2025, the National Assembly approved amendments to the Geology and Mineral Law, which reaffirmed the export restrictions of raw rare earth ore and introduced tighter limits on refined rare earth exports and planned to expand domestic processing. The changes aim to retain more value within domestic supply chains and strengthen Vietnam's downstream processing and manufacturing capacity.

The approach also aligns with the Comprehensive Strategic Partnership with the EU which includes cooperation on critical minerals and semiconductors. This multi-partner strategy choice will enable Vietnam to maintain leverage and flexibility over resource development and supply chain partnerships.

Thailand: Electric vehicle, battery hub ambitions and emerging upstream risk

Thailand has modest critical mineral resources, but it is the second-largest EV market and a major automotive assembly base in Southeast Asia. Thailand’s critical minerals MOU with the US, signed in October 2025, spans the entire value chain from exploration to recycling. It contains a “first opportunity to invest” clause for US companies, which Thai officials emphasise is non-binding and subject to domestic law.

So far, it is unclear whether Thailand’s bid to establish downstream EV and battery manufacturing will attract the level of US investment needed to significantly reorient supply chains away from their current deep integration with Chinese EV manufacturers, battery producers and component suppliers.

In practice, Thailand aims to play a competitive advantage role as a hub for downstream processing and EV assembly rather than as a partner for raw-materials. Nevertheless, recent geological surveys highlighted that Thailand could become a more significant rare earth player than is generally recognised, with an estimated annual of around 13,000 tonnes of rare earth oxides, primarily in northeastern Thailand. Current estimates place Thailand’s critical mineral reserves in the tens of billions of US dollars, although the underlying data remains limited and contested.

This emerging upstream role sits uneasily alongside the narrative of Thailand as a purely resource-light partner in the US critical minerals strategy. Civil society organisations and Mekong-focused networks have raised concerns that the expansions of rare earth exploration and processing could put ecologically sensitive areas under greater pressure, and create new risks of extraction, particularly in parts of the Mekong region where oversight remains insufficient. Without stronger commitments on upstream governance and downstream financing, Thailand risks increased extractive pressures while remaining reliant on existing supply chain structures.

Do the bilateral agreements add up to something larger?

Bilateral MOUs and ARTs have a common structural weakness. As largely non-binding agreements, they do not provide much clarity on coordinated price support. US-aligned mineral projects may therefore struggle to compete with Chinese-backed producers, who can sustain lower prices through subsidies and other supply-chain support. This makes it harder for these projects to remain commercially viable.

To address this issue, the US introduced FORGE (Forum on Resource Geostrategic Engagement), a multilateral framework designed to coordinate these arrangements at scale. FORGE aligns pricing and trade policy across US-aligned critical mineral supply chains. It engages several ASEAN states on critical minerals, complementing bilateral arrangements with a shared approach to price and trade governance. Rather than operating as a bilateral resource partnership with Southeast Asian governments, FORGE sits above and supports country-by-country arrangements.

Launched on 4 February 2026 at the Critical Minerals Ministerial in Washington, with 54 countries and the European Commission in attendance[5] it built on earlier initiatives such as Biden’s Minerals Security Partnership, which delivered quite limited projects. FORGE’s core mechanism and functions centre on coordinated reference pricing and price support measures across mining, processing and manufacturing. In terms of implementation, it is expected to involve tariff-based instruments. These measures aim to provide price stability and collective leverage across the supply chain. However, the design of tariff-based mechanisms relies on clarity regarding the tariff authorities under recent US trade measures, especially following US Supreme Court rulings.

Those rulings have narrowed the executive’s authority to impose tariffs, meaning current measures depend on time-limited statutory tools. This reliance on time-limited tariff authority creates a mismatch between mining and processing investments that require 10–20-year horizons. Therefore, the credibility of tariff-based price support mechanisms may remain weak.

Each bilateral agreement is arranged on a country-by-country basis. For example, in Indonesia there is the tariff relief, rare earth access in Malaysia, and processing incentives for the Philippines. At the country level, these agreements aim to address specific bottlenecks. More broadly, these agreements remain exposed to tense price competition, with China exerting significant influence over mineral and processing prices through state support, including subsidies. This enables Chinese-linked projects to undercut competing ventures across stages of the value chain, even where bilateral agreements include provisions on processing or investment.

In essence, the link between FORGE and the Southeast Asian agreements remains tenuous. There is still not enough clarity on unified ASEAN engagement related to FORGE, no common regional definition of “critical minerals”, and national strategies remain fragmented and often pulling in different directions across countries. In addition, Domestic policy implementation varies widely, from the Philippines’ “China-free” nickel ambitions to Indonesia’s Chinese-dominated processing base.

What remains unaddressed in the US critical minerals arrangements in Southeast Asia?

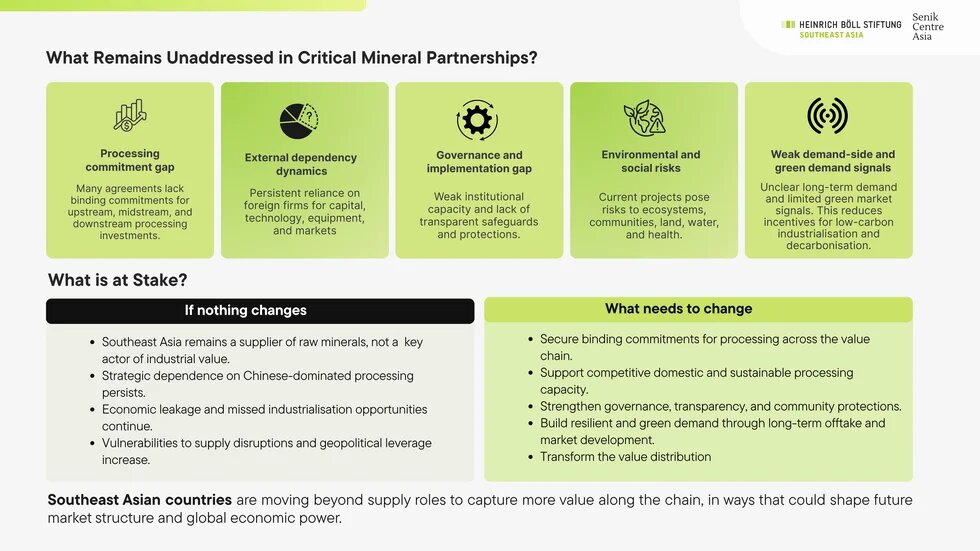

Recent US critical minerals agreements in Southeast Asia are largely focused on strengthening the supply chain and enabling investment and broader economic cooperation. However, both bilateral and multilateral arrangements leave certain structural constraints unaddressed:

- The processing commitment gap. MOUs between the Philippines, Malaysia, and Thailand signal interest in building domestic processing, but lack of binding investment commitments, technology-transfer requirements, and enforceable timelines. Without such obligations, these partnerships are unlikely to transform the value addition process and may instead perpetuate existing extraction patterns.

- External dependency dynamics. The expansion or diversification of critical mineral downstream processing has not necessarily reduced reliance on external capital, technology or market access. In many cases, this effort is added to existing industrial and financial structures rather than replacing them. Indonesia is a clear example of this. Although Indonesia’s downstreaming policy has increased nickel export values by more than tenfold in less than a decade, much of this growth is highly dependent on China. The Agreement on Reciprocal Trade (ART) requires Indonesia to open up more of its minerals sector to US investment, which could constrain future cooperation with China. It may create tension with Indonesia’s long-standing “free and active” foreign policy, and could limit Indonesia’s ability to maintain future investment and partnership.

- A governance and implementation gap. The pace of US deal-making (more than 20 bilateral agreements made in just five months) has outpaced the development of the governance frameworks required to oversee the risks associated with extraction and processing. Across the agreements, provisions related to environmental safeguards, labour standards, and community protection are typically poorly defined and not incorporated into enforceable commitments or operational frameworks. As a result, these arrangements have limited influence over project-level practices and depend heavily on domestic policy or regulatory systems.

- Environmental and social safeguards. Critical mineral expansion both extraction and processing may have significant environmental, labour and community impacts, yet these issues are not given much attention in current agreements. In Indonesia, many studies of the Morowali and Weda Bay industrial zones document the extensive overlap between nickel concessions and primary tropical forests, as well as large-scale land clearing, the build-out of coal-fired power plants, and environmental contamination. China Labour Watch has recorded at least 77 deaths and 120 injuries at Chinese-invested nickel plants in Indonesia between 2016 and 2024.

In the Philippines, Global Witness data show that the country is the Asia’s deadliest in Asia for land and environmental defenders, with 298 killings recorded between 2012 and 2023, many of which were linked to conflicts related to mining projects. A coalition of 35 civil society organisations warned in submissions to the US Trade Representative (USTR) that current agreements risk throwing standards that protect people and the environment. -

Weak demand-side commitments and price premiums signals. While the arrangements aim to secure supply, it provides limited clarity on long-term offtake, pricing structures, or guaranteed market access for processed materials. Crucially, it does not establish strong incentives for lower carbon production on the demand side, such as preferential procurement for low-carbon materials, green premiums, or carbon-differentiated standards, or price-support mechanisms linked to emissions intensity.

With limited certainty about future demand and price premiums for low-emissions products, the critical minerals sector has little pull factor to prioritise cleaner processing technologies. This is particularly evident in the most carbon-intensive parts of the supply chain, where decarbonisation requires significant upfront capital costs and significant technological upgrades.

What will shape the outcomes of these partnerships?

These partnerships have so far extended the US’s access to critical minerals, but have not fundamentally altered the distribution of value and risks across chains. Higher-value activities remain concentrated in advanced economies, whilst many of the environmental and social costs associated with extraction and processing continue to be borne by producing countries, which retain only a small share of the added value. The long-term outcomes of these partnerships will depend on several factors:

First, whether commitments to domestic processing are matched by investment, technology transfer, and implementation measures that could improve the industry. Although the MOUs signed with the Philippines, Malaysia, and Thailand encourage domestic value addition, they do not require investment in processing capacity before export. This gap may affect whether these commitments translate into real, sector‑level change.

That such arrangements with lack of binding investment commitments, technology transfer, and timelines, risk perpetuating rather than transforming exploitative patterns. By contrast, the US–Australia framework included commitments from each government to provide US$1 billion in project financing within six months, with the capital and timelines defined from the outset.

Second, whether US policy support can endure across administrations. Recent Supreme Court rulings have narrowed the executive’s ability to impose broad tariff authorities, emphasising the need for clearer congressional support for long-term mineral policy. Yet the political path remains unsettled, and the future direction will continue to depend on political priorities. The mismatch between a short policy cycle and a longer timescales required to develop processing capacity means that support based on tariffs is less reliable for long-term project planning.

Third, how producing countries use policy space to shape outcomes. Indonesia’s commitment to downstreaming, Malaysia’s decision to maintain its ban on raw rare earth export, and Vietnam’s choice to sign only a framework agreement all suggest a willingness to use leverage to protect domestic industrial strategies. Those retaining tighter control over export rules and processing requirements will preserve greater bargaining leverage, even where outcomes remain uneven.

At the regional level, however, these approaches remain fragmented. Agreements proceed on a country-by-country basis, with no common ASEAN position or shared definition of critical minerals. This fragmentation could hinder the coordination across standards, incentives, and export rules, making it more difficult to improve safeguards and push more value addition across the region.

Oxfam study on the energy transition’s political economy indicates that Global South countries hold around 70% of identified transition mineral reserves while capturing only a small share of the value created further up the chain. Southeast Asian producers are on a similar trajectory. They supply the raw materials needed for the production process, while value accrues in downstream segments of the supply chain, particularly in established industrial and processing hubs such as China and in major end-market economies such as the US. This pattern is likely to persist unless commitments move beyond signalling intent towards binding investment, processing, and market access.

Fourth, transformation in value distribution. This depends not only on the design of agreements, but also on how domestic institutions implement policies through regulatory and permitting processes. Without greater coordination across producing countries and stronger control over processing, investment and market access, policy space alone is unlikely to result in an equitable distribution of value along the supply chain.

___

Senik Centre Asia is an independent think tank focused on climate, energy transition, and equitable development.

Disclaimer: This published work was prepared with the support of the Heinrich Böll Stiftung. The views and analysis contained in the work are those of the author and do not necessarily represent the views of the foundation. The author is responsible for any liability claims against copyright breaches of graphics, photograph, images, audio, and text used.

References

ABS‑CBN News. (2026, February 6). Philippines, US ink deal on mineral processing.

Antara. (2026). Indonesia prioritizes downstreaming in investment cooperation with the US.

Asian Peoples’ Advocacy. (2026). ASEAN, FORGE, and the risks of fragmented critical minerals governance (PU‑328‑IPAB‑V59‑WEB).

Atlantic Council. (2026). US critical minerals policy goes collaborative with FORGE.

Bloomberg. (2023, January 30). Philippines may tax nickel exports to follow Indonesia’s success.

Bloomberg. (2025, December 11). Vietnam amends law to ban exports of raw rare earth minerals.

Brookings Institution. (2026). Brookings experts on the Supreme Court’s tariff decision.

C4ADS. (2023). Refining power: China’s control of Indonesia’s nickel smelters.

CELIOS. (2026, March). CELIOS files formal objection to the Indonesia–US reciprocal trade agreement (ART).

CELIOS. (2026, March). Indonesia–US trade agreement challenged in court: Civil society coalition warns of risks to economic sovereignty.

China Labour Watch. (2024). Two worker deaths in three days at IMIP Indonesia.

Climate Rights International. (2025). Environmental and human rights violations at Philippines nickel mines.

Climate Rights International. (2025). New report shows human rights and environmental abuses at Philippine nickel mines.

Climate Rights International. (2026). The Philippines government should ensure the US thirst for minerals does not drive abuses.

Climateworks Centre. (2025). Decarbonising Indonesia’s high‑value industrial sites: Summary report.

Council on Foreign Relations. (2026). The Supreme Court clipped Trump’s tariff powers and opened new trade battle fronts.

CSIS. (2023). China’s new rare earth and magnet restrictions threaten US defense supply chains.

CSIS. (2025). Indonesian industrialization: Downstreaming the value chain.

CSIS. (2026). Critical minerals ministerial introduces new international cooperation strategy.

ECFR. (2024). Material world: How Europe can compete with China in the race for Africa’s critical minerals.

European Central Bank. (2025). China’s export controls on critical raw materials: Risks for Europe (Occasional Paper 384).

European Commission. (2025). Joint press statement on the EU–Vietnam comprehensive strategic partnership.

Global Trade Alert. (2025). China: Temporary suspension of additional export controls for rare‑earth‑related technologies.

Global Voices. (2025, April 7). How China’s investment in Indonesia’s nickel industry is impacting local communities.

Global Witness & Mongabay. (2023, September 6). Who were the 11 Philippines environmental defenders killed in 2022.

Guardian. (2026, March 2). Oil prices surge above $120 a barrel as Iran war shuts Hormuz shipping

Hinrich Foundation. (2025). Indonesia’s trade policy amid US–China rivalry.

Insider PH. (2026). Philippines, US seal deal on critical minerals development.

International Energy Agency. (2024). Global critical minerals outlook 2024.

International Energy Agency. (2025). Law on geology and mineral resources (Vietnam).

Jakarta Globe. (2024). How nickel industrialization is transforming Indonesia’s economy.

Krungsri Research. (2025). Rare earth: New strategic opportunity for Thailand.

Lynas Rare Earths. (2024). Lynas Rare Earths awarded new US Department of Defense contract.

Mining.com. (2025). US agency slashes its estimate of Vietnam’s rare earth reserves in major revision.

Mining Technology. (2024). Nickel in the Philippines: Country profile

Motor. (2024, December). Materials and battery supply chains ready to meet future global EV demand.

Nation Thailand. (2025). New geological surveys highlight Thailand’s rare earth potential.

Oxfam. (2023). Unjust transition: Reclaiming an energy future from climate colonialism.

Philippine Embassy in Washington, D.C. (2026, February). Philippines signs MOU on critical minerals supply chains.

Quest Metals. (2025). Malaysia’s ban on raw rare earth exports.

Reuters. (2025, April 4). China hits back at US tariffs with rare earth export controls.

Reuters. (2025, October 26). US and China sign trade deals with Cambodia, Malaysia, Trump says.[new from your list]

Reuters. (2025, December 11). Vietnam curbs exports of refined rare earths, reaffirms ban on ore trade.

Resource Trade Earth. (2023). Critical metals for EV batteries

SAIS Review. (2025). Unearthing influence: China’s global strategy for transition minerals.

ScienceDirect. (2023). Lynas and Malaysia’s contested role in rare earth supply chains.

ScienceDirect. (2023). Decarbonising energy‑intensive mineral processing.

Senik Centre Asia. (2026). Analysis of US–Southeast Asia critical minerals agreements and processing policies [Internal analysis].

Signal Group. (2020). Philippine nickel ore ban reversed: What are the impacts?.

SP Global. (2025). China’s Africa battery‑metals supply chain build‑out.

Stanford University. (2024). Confronting China’s grip on graphite for batteries.

Statista. (2024). Countries with the largest known rare earths reserves.

Thai PBS World. (2025). US claims intent of Thai–US rare earth MOU as cooperation, not control.

Tilleke & Gibbins. (2025). Thailand’s critical minerals MOU with the United States.[new from your list]

Trading Economics. (2025). Indonesia exports to China: Nickel.

U.S. Congress. (2024). International trade: Tariff schedules and investment rights (CRS Report R48676).

U.S. Congress. (2026). The Supreme Court’s tariff decision: Implications for trade policy (Legal Sidebar LSB11398).

U.S. Embassy & Consulates in Indonesia. (2026). Fact sheet: Trump administration finalizes trade deal with Indonesia.

U.S. Mission to ASEAN. (2026). 2026 critical minerals ministerial.

U.S. State Department. (2025). Minerals Security Partnership.

U.S. State Department, Office of the Spokesperson. (2026). Opening remarks of the Critical Minerals Ministerial.

U.S. Trade Representative. (2026). Agreement between the United States of America and the Republic of Indonesia on reciprocal trade (ART).[Office homepage https://ustr.gov/]

USASEAN Business Council. (2025). Malaysia’s critical minerals MOU with the United States draws Chinese counter‑proposal.

USGS. (2021–2026). Mineral commodity summaries: Burma, rare earths, cobalt

Visual Capitalist. (2024). China’s grip on critical mineral refining.

VOI. (2024). Only 10% of nickel profits accrue to Indonesian companies.

White House. (2025, October). Fact sheet: President Donald J. Trump secures peace and prosperity in Malaysia (section on framework agreement with Vietnam).

White House. (2025, October). Memorandum of understanding between the Government of the United States of America and the Government of Malaysia concerning cooperation to diversify global critical minerals supply chains and promote the energy transition.

[1] In order to accommodate the ongoing discourse around the global mineral supply chain issues, this briefing uses the terms “transition minerals” and “critical minerals” interchangeably.

[2] The States Policies Scenario refers to the IEA's projection on the direction of the global energy system based on the current policies that are already in place or have been officially announced.

[3] The IEA's scenario refers to a normative pathway for achieving net-zero energy sector emissions globally by 2050. This is consistent with limiting global warming to 1.5°C.

[4] Indonesia think tank CELIOS highlighted that in the agreement “Indonesia shall” clause appears more than 200 times across the 45-page text, compared with only nine instances of “United States shall” a 22-to-1 ratio of obligation.

[5] Founding members include South Korea (chair through June 2026), Japan, Australia, the United Kingdom, Canada, Angola, the Democratic Republic of the Congo, andtechnology-transfer Ukraine, alongside Southeast Asian partner.