Article

President Ferdinand Marcos Jr. of the Philippines immediately signed into law the controversial Maharlika Investment Fund (MIF) bill on July 18, 2023. The MIF will establish a diversified portfolio of investments in local and global financial markets, real estate, infrastructure projects, and other assets that promote its objectives. Investments may include cash, foreign currencies, fixed income instruments, equities, Islamic investments (Sukuk bonds), mutual funds, and joint ventures.

The Maharlika Investment Corporation (MIC), a government-owned and -controlled corporation (GOCC), will be responsible for governing and managing the MIF. The MIC will be governed by a Board of Directors. It will adhere to the Santiago Principles and other internationally- accepted standards of transparency and accountability. The MIC will coordinate with relevant institutions to ensure harmonization of policies. It will have an authorized capital stock of five hundred billion pesos divided into five billion shares, with common and preferred shares. The initial capitalization will come from the National Government, Land Bank of the Philippines (LBP), and Development Bank of the Philippines (DBP).

The final idea of the MIF is difficult to capture even in the Republic Act No. 11954 that creates it and the MIC that will run it. The Department of Finance (DOF) provides a clearer and more coherent rendition of the purported aim of the law: The Fund will catalyze economic development and accelerate the country’s growth by optimizing the use of government financial assets and promoting their intergenerational management. The Fund will accelerate infrastructure development in the country, create a lot of high-quality jobs, attract more foreign investors, and propel the country toward higher growth.

The MIF will complement the government’s existing mechanisms to finance priority projects in pursuit of the government’s goals in the Philippine Development Plan, the 8-Point Socioeconomic Agenda, and the Medium-Term Fiscal Framework. The MIF will widen fiscal space, ease the burden on local funds, and reduce reliance on official development assistance in funding, e.g., Infrastructure Flagship Projects (IFPs).

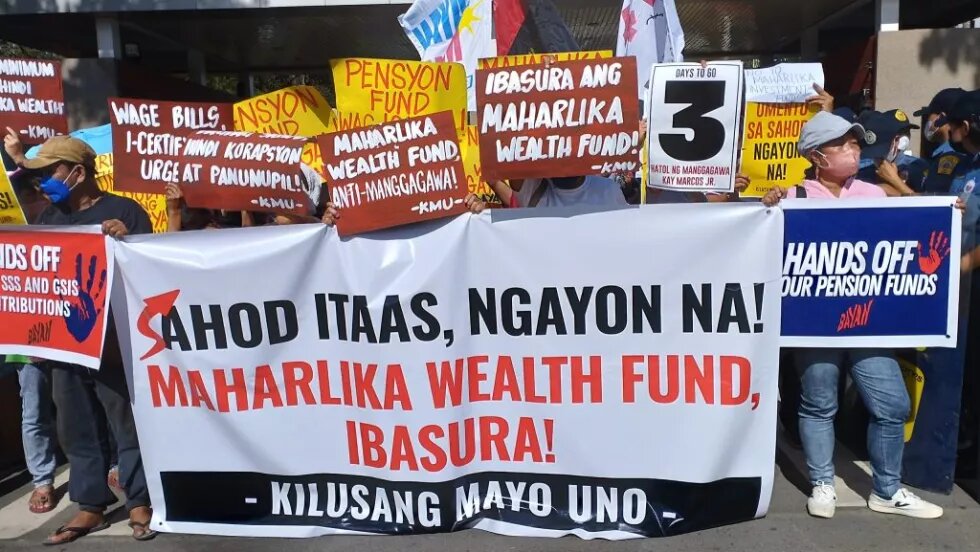

The main concerns raised by academia, the business sector, civic groups, and the media on the purpose, timing, source of funds, risks, and management of the MIF include the following:

- Unclear and Contradictory Goals: The stated goals of the MIF have changed and are now so broad they are subject to discretionary focus and interpretation by the MIC.

- Independence from National Plans: The MIF adherence to the Philippine Development Plan and the Medium-Term Fiscal Framework is assumed but has not been explicit or elaborated on.

- Unproven Effectiveness: The MIF lacks evidence to suggest that it will generate additional investment and economic activity beyond what would naturally occur in its absence.

- Impact on Financial Stability: Jeopardizing the funding sources like DBP and Land Bank could reduce their lending capacity, affecting farmers and micro-entrepreneurs with a significant reduction of approximately P750B. The financial resources of the BSP are essential for responding to financial crises and should be safeguarded.

- Governance and Feasibility Doubts: The governance structure, exemptions from regulations, and compatibility with the current global environment raise serious doubts about the feasibility of the MIF.

- Lack of Consensus: The MIF lacks sufficient genuine consensus among critical stakeholders, with doubts remaining among business, academia, and the public.

Generally, private sector opinion of an unsound Presidential brainchild is expressed privately, in contrast to legislators and politicians who exude exaggerated support. But in the case of the MIF, as early as December 2020, 12 organizations of economists, businessmen, and think tanks opposed House Bill No. 6398 -- the early version of the MIF -- which called for the creation of a sovereign wealth fund. The statement said the MIF ran contrary to the principles of fiscal prudence, pension fund solvency, Bangko Sentral ng Pilipinas (BSP) independence, good governance, and transparency. The 12 signatories were the Foundation For Economic Freedom, Competitive Currency Forum, Filipina CEO Circle, Financial Executives Institute of The Philippines, Institute of Corporate Directors, Integrity Initiative, Inc., Makati Business Club, Management Association of The Philippines, Movement for Good Governance, Philippine Women’s Economic Network, UP School of Economics Alumni Association and Women’s Business Council Philippines, Inc.

Former Bangko Sentral ng Pilipinas Deputy Governor Diwa C. Guinigundo, who subscribed to the above statement, went on to write to the senators on the Maharlika Investment Fund to underscore that there is nothing in the MIF to promote economic growth and social development that is not presently undertaken by existing public institutions in collaboration with the private sector.

Several international investment experts like Stephen Cuunjieng have been outspoken in most talk shows and fora available to him, warning of the defects and dangers of the MIF, primarily in that it handicaps the Land Bank and the Development Bank of the Philippines by reducing their equity which translates into a tenfold reduction in their capacity to lend to small borrowers in the country. The Central Bank's monetary stewardship role would also be weakened by the periodic transfusion of dividends to fund the MIF.

For his part, Bob Herrera-Lim, an expert from a U.S. consultancy firm, presents the most profound insight – the Maharlika Investment Fund, no matter how well-intentioned, cannot rise above the general weakness in institutions and governance in the Philippines.

It is clear that Marcos Jr. has owned the MIF idea early in his first year in office, with his Finance Secretary Benjamin Diokno being the most avid promoter and defender of the MIF idea.

The investment fund idea is not entirely new; it has been explored during the administration of Pres. Benigno Aquino III but was apparently not deemed feasible or timely. Being investment strapped, the Philippines has looked at various investment generation and attraction mechanisms, the Norway Sovereign Fund being among the most cited. The Philippines, however, did not have "surplus" funds, so the Indonesia model seemed to be the most practicable.

Marcos Jr. has taken a bold, counter-intuitive move. The Maharlika Investment Fund reminds people too easily of the cronyism and grand financial schemes, like the Coco Levy and the virtual Marcos control of the Central Bank of the Philippines, that Marcos Sr. implemented, mismanaged, and caused his downfall. Will Marcos Jr’s Presidential leadership spell the difference between failure and success despite a changeless political, economic, and social context?

The MIC as a government-owned and controlled corporation (GOCC) cannot, except perhaps in the initial phases, set itself apart from the character and performance of the larger bureaucracy that will manage and implement the development projects envisioned under the MIF. Marcos swims against the current of economics and finance wisdom as expressed by experts.

The real test of success and sustainability is whether the MIF will attract foreign investments which must come in droves soon if the domestic naysayers will be forced to change their tune. This is not within Marcos Jr.’s control, except perhaps the investment of the famed Marcos hidden wealth. As of the end of 2020, the Philippine government has recovered P174.2 billion in the Marcos ill-gotten wealth. The Presidential Commission on Good Governance before the last Presidential elections was still running after P125.9 billion.

Still, the country's relatively weak investment climate compared to Vietnam and Thailand may induce a wait-and-see attitude among foreign investors. The remaining five years of Marcos' term may not provide sufficient runway for the MIF to take-off. No matter how successful, Marcos can most likely only equal the economic performance of President Benigno Aquino III. Without a clear programmatic succession scenario to sustain the gains, the likelihood of another populist Duterte squandering the gains is high. The view from the outside the Philippines is different from what Marcos naively wishes it to be.

The MIF promises to be a huge gamble the Philippines, under the Marcos Jr. presidency, is attempting. It is an uncharted, unprecedented move. But the MIF is also an issue of public confidence in the Marcos Administration. Ferdinand Marcos Jr. being scion to the Marcos Administration that was chased out of by People Power in February 1986, suffers from a deeply nurtured sense of public distrust, especially among the elite. The Maharlika Investment Fund, which Marcos proposed early in his administration, has become the proxy policy for this issue of trust that will likely linger like a shadow.

The State of the Nation Address (SONA) of President Marcos Jr. on July 24 provides a critical context of the MIF going forward. That SONA, delivered in 75 minutes, was an eye-opener to the earnestness of this President to carve a credible developmental agenda for the nation. He deftly unfolded a comprehensive tapestry of the accomplishments and efforts of the wide bureaucracy in addressing the people in a resurgent post pandemic situation.

The claims were often extravagant. Some were outright dubious, like the hopes pinned on the Marcos Sr. regime-era Kadiwa Centers that are now claimed to have significantly eliminated the middleman in the transactions between farmer producers and food consumers. The uncritical passing on by Marcos Jr. to the public of what was submitted to him by the bureaucracy is a disturbing tendency that creates incredulity rather than confidence.

But still, the SONA showed Marcos Jr. as a "normal" Philippine President. This normalcy of the Marcos Jr. presidency is not only in contrast to the preceding grotesque presidency of Rodrigo Duterte in terms of style and content of leadership, management, diplomatic, and stakeholder engagement. It also harkens to the businesslike Presidency under Corazon Aquino, Fidel Ramos, Gloria Arroyo, and Benigno S Aquino, with the Joseph Estrada and Duterte presidencies as outlandish outliers.

Even before it became law, Marcos already “soft-launched” the half-cooked MIF in the World Economic Forum in Davos, Switzerland in January 2023. Once it became law, Marcos Jr. has gone on to promote the Maharlika Investment Fund in his recent state visit to Malaysia, where the most recent sordid misuse of the sovereign fund mechanism had occurred under the term of former Prime Minister Najib Razak. Marcos Jr. reports that Malaysian businessmen and investors are very positive about the MIF and are considering investing in it. That would indeed be a coup if it happens, turning the minds even of jaded Filipinos.

Marcos Jr. seems bent not only in treating the MIF as an investment challenge, but also as a public trust challenge. Despite the investment context and fundamentals being perceived as bleak, President Marcos Jr. still stakes his Presidency on this flagship policy issue.

Meanwhile, the MIF can also be the flagship issue that could enliven and embolden the re-emergence of a civil society movement for transparency and accountability. The opposition still seems shell-shocked by the results of the May 2022 elections, and have not self-mobilized since. The midterm elections of half the Senate, the whole House of Representatives, and all local government posts will happen in May 2025, but there are no visible opposition efforts at self-mobilization around key issues like the MIF, corruption, food and energy security, and inflation.

Now that the law is in play, whether it will be a boon or bane to the Filipino people depends not only on the competence and integrity of the Marcos administration, his capacity to effectively control and wield a wayward bureaucracy, and the vigilance of the people. Civil society organizations could demand more transparency and accountability from the administration and goad institutions like the Ombudsman, the Sandiganbayan, and Congress to exercise and exact more transparency and accountability.

The atmosphere of the rule of law and civic participation in the Philippines, however, is vigorous in procedures but extremely anemic in spirit. There is a pall of self-censorship and intimidation that has lingered from the previous administration. The cases of former Senator Leila de Lima, the outlandish termination of the franchise of ABS-CBN, the continuing pushback of the government on the ICC investigation of the Duterte war on drugs, and the continuous stonewalling on the citizen request for transparency in the transmission logs during the last elections indicated the unwillingness of Marcos Jr. to completely break from the excesses of the Duterte administration.

From the wider context of politics in the Philippines, the MIF demonstrates the power of the Presidency in setting government policy regardless of a widespread opposition. Another President would have backed down. That President Marcos Jr. has set his mind on the MIF demonstrates either a capacity for strategic vision, or a wanton disregard of public opinion. For most Filipinos, this looks like strong Presidential leadership, and they are happy with it. In the context of the quality of democracy in the Philippines, this lack of a critical citizenry at this juncture is really the boon or bane issue.

__

Dr. Segundo Joaquin E. Romero, Jr. is a fellow with Future Earth Philippines and a lecturer at the Development Studies Program of the Ateneo de Manila University.

The views expressed in this article are not necessarily those of Heinrich Böll Stiftung.