Dependence on fossil fuel in ASEAN countries has increased rather than decreased. Fossil fuels draw on finite resources that will soon dwindle, becoming more and more expensive and damaging the environment. In contrast, renewable energy– wind, solar, geothermal and biomass– promises a future with clean energy sources which will have a lower environmental impact and will not run out. Instead of spending large amounts on energy input and systems, most renewable energy investment is spent on materials and workmanship to build and maintain facilities. This means that the energy money could be used to create jobs and promote local economies.

In the face of dramatic economic growth, population growth and climate change, over 160 million ASEAN residents still do not have access to electricity. Speeding up the development process of renewable energy would seem to be the right solution to solve ASEAN energy issues. With abundant renewable energy sources, it is time for renewable energy to flourish in ASEAN to prevent problems such as energy shortages, global warming emissions, and protect citizens’ health, the environment and the climate.

Upcoming Challenges in Energy Demand— the Regional Imbalance of Energy

While the ASEAN region is usually known as a rich natural energy region in the world, some countries in ASEAN perform quite poorly with regard to energy resources. According to the World Bank Database (2016), 4 out of 10 countries in ASEAN are energy importing countries including Singapore (98%), the Philippines (46%), Thailand (42%) and Cambodia (33%). Singapore is mentioned as one of the eight economies without energy resources in the world[i], and is completely dependent on imported energy. Cambodia’s imported diesel fuel accounts for 90% of domestic electricity production[ii]. In general, these countries have strongly relied on imported fuels, so they are prone to feeling the effects of rises in fuel prices and easier experiencing supply shortages than the others.

Meanwhile, other countries such as Brunei, Indonesia, Myanmar and Vietnam are well known for exporting energy resources. These countries, whose main source of income is commercial energy, will continue to provide important energy resources to other countries in the region. For example, Brunei produces approximately 127,000 barrels of oil per day and 243,000 barrels of oil equivalent of natural gas per day,[iii] of which 24.3% is exported to Singapore[iv]. However, a surprising fact is that exporting countries are not able to provide for their own needs. For example, Vietnam is known as a coal exporter, but has not been able to supply enough coal for its own needs in the recent years due to the exhaustion of high quality coal. Ironically, this has lead the country to experience energy shortages. With the exception of Brunei, all ASEAN countries are projected to be energy deficient.

There is still a gap in the ASEAN energy system supply and demand. Some countries generate a surplus of energy, while others are falling into an energy deficit. Electricity demand in Laos only reaches 27% of the total power supply. Therefore, instead of being a big concern for power security, Laos’ government is interested in the commercial aspect of power, which could bring many benefits to the country. For example, Laos could capitalize on the power grid, which has been growing in the region in recent years. Meanwhile, only 35% of Cambodians have access to grid electricity. Moreover, they are even subjected to high power prices, which are among the highest in the world.

Environmental Problems from Energy Usage in ASEAN

The industrial revolution in the region led to an exponential increase of energy consumption, which in turn has caused a lot of damage to the environment. Due to remarkable economic growth along with a rapid urbanization growth rate over the past three decades, ASEAN’s growth has required a huge consumption of energy. Many environmental problems such as water pollution, air pollution, deforestation and land degradation are caused by energy production and consumption. Air quality has experienced a dramatic deterioration due to greenhouse gases (GHG) from industrial processes. Transportation in urban areas is increasing, especially in metropolis areas like Manila, Jakarta, Bangkok and Ho Chi Minh City. Fresh water concerns have become a bigger topic due to the increase of waste from thermal power plants. Several ecological problems have appeared due to hydroelectric power plants, threatening the ecosystems of several lakes and rivers in Laos, Vietnam and Cambodia.

Furthermore, ASEAN is one of the most vulnerable regions to climate change impact, which is considered a consequence of the worldwide industrial revolution. In recent years, several ASEAN countries have suffered from natural disasters such as droughts and rising sea levels (Vietnam), typhoons (Vietnam and the Philippines), earthquakes (Myanmar) and tsunamis (Indonesia and Thailand). Therefore, ASEAN countries have to face the environmental consequences of their extensive energy use as well as the accelerated energy consumption growth worldwide. They have to take a stand on crucial issues, which support further economic growth but also have serious environmental repercussions.

The Tides are Changing in Favor of Renewable Energy

The world remains hopeful about renewable energy. Since 2015, the term “100% renewable energy” has become increasingly commonplace and is mentioned frequently. Moreover, we have seen the emergence of 100% renewable electricity[v] in 14 countries such as the US, Austria, Germany, UK, Canada, Denmark, etc. In 2015, Sweden challenged other nations to follow suit and use 100% renewable energy[vi]. Renewable energy is growing every day. After the 2016 UN Climate Change Conference in Marrakech, Morocco, 48 members of the forum vowed to use 100% renewable energy by 2050[vii]. Australia is one of the first countries to set a high renewable energy target. Its national target of 23.5% renewable energy by 2020[viii] was announced in 2015 as a part of the Government’s reforms to the Renewable Energy Target (RET). However at the federal level, there is a unique example of the Australian Capital Territory (ACT), in 2016, the ACT government switched the target to 100% renewable energy[ix]. In 2017, as a leader in renewable energy, the ACT government confidently stated that there would be no technical impediments to reaching their target of 100% renewable energy which can place Canberra at the lead in Australia and internationally, of cities taking effective action on climate change[x].

Many countries have shifted or are starting to shift to 100% renewable energy in particular sectors such as electricity, heating and cooling, and transportation. All of them assert that renewable energy is no longer a thing of fantasy, and ASEAN, indeed, is a part of this transition.

The Future of Renewable Energy is Getting Brighter in ASEAN

Let us ask a few practical questions regarding the future of renewable energy in ASEAN. What is the renewable energy potential in ASEAN countries? Are they prepared for the renewable energy market? What about the costs, mechanisms, policies and market support for renewable energy in the region?

Renewable Energy Potential in ASEAN

According to a report from the ASEAN Centre for Energy in 2016[xi], ASEAN is richly endowed with diverse renewable energy sources such as biomass in Thailand, huge geothermal potential in Indonesia and the Philippines. Moreover, located close to the equator, the amount of sunshine throughout the year could bring a significant amount of solar potential. Wind potential has also been a focal point in the past several years. The significant potential of wind power is reported in Thailand, the Philippines, Vietnam and Indonesia. In light of the rapid growth of renewable energy technology and a subsequent decline in renewable energy costs, it could lead the region to move away from traditional energy resources and centralized utility models to supply energy.

For example, Laos’ energy sources are mainly traditional fuels including various biomass sources. These biomass sources include both wood and charcoal. According to a report from the Laotian Government[xii] in 2011, biomass energy accounted for 69% of total energy consumption, fossil fuel accounted for 17%, electricity accounted for 12% and coal accounted for 2%. For the whole energy supply, potential of biomass, biogas and organic waste are estimated as the important energy resources. Specifically, there is around 4100 MW of power potential from renewable energy including approximately 1450 MW from biogas, biomass and solid waste production, and 500 MW from solar.

Meanwhile, biomass could also become a diesel fuel substitute in Cambodia. Wind power is estimated at 3,665 GWh/year, and solar power is evaluated at 65 GWh per year for technical potential in the country[xiii].

According to Dr. Doan Van Binh, Director of Institute of Energy Science – Vietnam Academy of Science and Technology, the total potential of wind power in Vietnam is estimated at 513,360 MW, which equivalent to more than 200 times as much as power capacity of the biggest hydro power plant in Vietnam. PV power is stable during the year with around 2000-2600 sun hours per year and only reduces about 20% in the rainy season from the 17th parallel to the south. This number is lower at 1500-1700 sun hours per year in the rest of the country[xiv].

Other countries such as Indonesia are regarded as some of the largest geothermal countries in the world, with 299 geothermal locations and a total potential of 28,897 MW. This accounts for around 40% of total geothermal resources worldwide[xv].

Supporting Renewable Energy Development from the ASEAN Governments

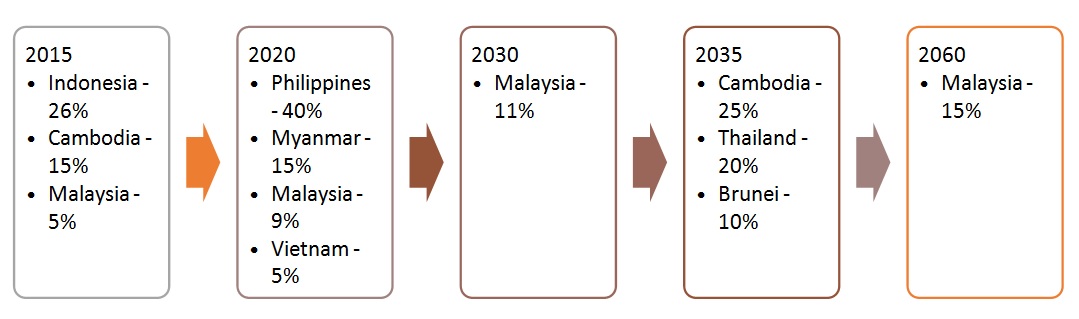

In recent years, ASEAN governments have created many short–premium–long schemes to develop renewable energy. ASEAN as a whole, as well as individual countries, set up the schemes based on renewable energy development targets. Each target was established as a share of the renewable energy power supply (see fig. 1), primary energy and final energy consumption. They include large-scale hydropower, but do not include renewable energy in the traditional form of firewood. All countries in the ASEAN region agreed to meet the target of 23% renewable energy by the year 2025. Laos’ government announced its own target in 2015 to meet 30% renewable energy by 2025. In that same year, Indonesia expects to achieve 25% and Vietnam expects 8% of their energy supply to be renewable energy[xvi].

Fig 1. Targets for the share of renewable power supply in ASEAN countries.

Source: ASEAN Plan of Action for Energy Cooperation (APAEC) 2016-2025.

As leaders in the region for renewable energy loyalty, Indonesia has completed guidelines for biomass, biogas and small hydropower, and Myanmar has also announced its guidelines. Malaysia completed its guidelines for small hydropower as well as solar implementation, while the Philippines and Vietnam finalized their guidelines for solar power in early of 2017[xvii]. Although each country has diverged from each other in terms of renewable energy, they still collaborate with each other. One such joint effort was the common target and roadmap called Remap Options for a Clean, Sustainable and Prosperous Future[xviii]. This roadmap provided a breakdown of renewable energy potential by sector and source, and established guidelines to achieve all targets.

ASEAN Renewable Energy Markets – How to Unlock the Potential?

Although ASEAN has an advantage when it comes to abundant resources, it remains to be seen whether the region will be able to tap into its potential. The majority of renewable energy sources remain untouched in ASEAN. For example, looking at individual countries, only 2MW of 65GWh technical potential of solar power has been installed, while biomass and wind power are underused in Cambodia. Indonesia only utilizes 5% of its geothermal potential. With the exception of the Philippines, currently in the lead with 400MW of wind energy, wind power remains a door left open for other ASEAN countries.

In the whole region, only 51 GW or 26% of the power supply is generated from renewable energy resources, including large hydropower (2014). Without hydropower, this figure was at a mere 5% in 2014— a surprising number in comparison to the calculated potential in the region. Details of the renewable energy status in each ASEAN country can be seen in figure 2.

Fig 2. The renewable energy status in ASEAN countries from 1995 to 2014 - IEA[xix]

It is yet to be determined whether ASEAN could be a promising renewable energy market. ASEAN is on its way to becoming a driver of global development with an increasingly high economic growth rate. Along with this, the explosion of urban cities and the nonstop population growth in the region could bring both great challenges and opportunities in terms of renewable energy development. Thus, ASEAN could learn how to turn potential into reality from other countries and regions such as the European Union, the US or Japan.

Considering the size of ASEAN, the EU currently has more economic power, which is further developed and well-equipped for renewable energy policies. ASEAN could use their dynamic economy as a selling point to attract more investment, as well as to save time by applying practices from the EU while developing their renewable energy market.

As leaders in renewable energy development, the EU and USA have demonstrated the efficiency of dividing the renewable energy market into segments. For example, the solar market in the EU is segmented into utility-scale systems, commercial and industrial rooftop systems, and residential application. In some countries such as the Czech Republic, the Netherlands, Denmark, Austria and Belgium, residential solar power represents a substantial share of the solar market. Other countries such as Germany, Slovakia and Switzerland recorded a great share of solar power consumption in the commercial sector. Therefore, capital issues are divided equally among the people, and there is a more constant flow of capital dedicated toward the development of renewable energy. By comparing renewable energy markets in the EU, one could infer that the more widely-distributed markets such as Germany’s solar PV would be less likely to collapse the PV industry than focused markets such as the Czech Republic.

Thailand, the Philippines, Indonesia, Malaysia and Vietnam, the five big markets of solar PV, could learn to drive the market toward this trend. However, if awareness of clean energy remains low, and information on the benefits of renewable energy is limited, this is not likely to happen. Campaigning should be designed for people of all backgrounds including children, teenagers, students, building professionals and the general public. The actions could be diversified in games, competitions, debates, workshops and conferences, and exhibitions of real renewable energy applied models. One example is the 10ACTION project, which took place in Europe[xx] from 2010 to 2012. The project aimed to improve social acceptance, and was a case study in the Netherlands in 2015[xxi].

In order to develop a diverse energy market oriented towards segmentation, reducing renewable energy cost has to play an important role. The relationship between price and investments is a key market starting point. High risk, high reward is the main concept for all investors. However, for ASEAN energy markets, this does not seem so obvious due to the growing demand for power and renewable energy’s cost-competitiveness compared to other power options. ASEAN energy markets might have to find price levels where supply and demand is the least out of balance.

Fortunately, ASEAN countries may be able to save up to a decade in renewable energy development, especially through learning from the experiences in building energy market in developed countries. ASEAN could draw on past experiences and observe other markets to make this a possibility. It is easy to see similarities between the ASEAN and EU power grids. Instead of starting from zero, ASEAN countries could get a head start by learning from the energy market reform in Europe with fixed market mechanisms to produce the right price of carbon, modules of energy mix prices, etc.

Moreover, ASEAN countries have benefited from the rapid development of technology. In December 2016, the WEF reported that solar and wind were the same price or even cheaper than fossil fuels in more than 30 countries[xxii]. In February 2017, ABC News announced that solar energy in Australia was cheaper than retail power prices in most capital cities[xxiii]. The explosion of technological development is marking a turning point in renewable energy development. In November 2016, a new PV roof made by Tesla CTO JB Straubel proved to be less costly than a regular roof, even before energy production[xxiv]. The CEO of the company claimed that such technology could bring huge gains to the entire supply chain as well as to customers. With a huge potential of solar power, this new technology could be the right solution for ASEAN to solve the perception or high risk among investors and project developers. Additionally, this would also open the door for residential customers to equip their houses with solar PV.

Aside from profiting from renewable energy developing achievements of the world, ASEAN also needs to work together with other countries to solve energy storage issues. As renewable energy usage increases day by day, supporting greater amounts of renewables on the grid and ensuring the quality of electricity, energy storage is becoming the big question in both on-grid and off-grid systems.

References

[i] https://www.gamespot.com/forums/offtopic-discussion-314159273/8-countries-with-no-natural-resource-but-thrive-to-29364331/

[iv]http://www.ei.gov.bn/Lists/Energy%20News/NewDispForm.aspx?ID=58&ContentTypeId=0x010061E25E0862D5FC419D92E1307D83196C

[vi] https://cleantechnica.com/2016/02/04/how-11-countries-are-leading-the-shift-to-renewable-energy/

[vii] http://www.independent.co.uk/news/world/renewable-energy-target-climate-united-nations-climate-change-vulnerable-nations-ethiopia-a7425411.html

[viii] http://reneweconomy.com.au/act-lifts-2020-target-to-100-renewable-energy-as-australia-stalls-86177/

[xi] http://www.aseanenergy.org/blog/facing-the-challenges-on-energy-demand-time-for-renewable-energy/

[xii] Lao Government, Renewable Energy Development Strategy, Vientiane: Government, 2011.

[xvi] http://www.aseanenergy.org/resources/publications/asean-plan-of-action-for-energy-cooperation-apaec-2016-2025/

[xix] Database from IEA website: https://www.iea.org/

[xxii] https://qz.com/871907/2016-was-the-year-solar-panels-finally-became-cheaper-than-fossil-fuels-just-wait-for-2017/

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}